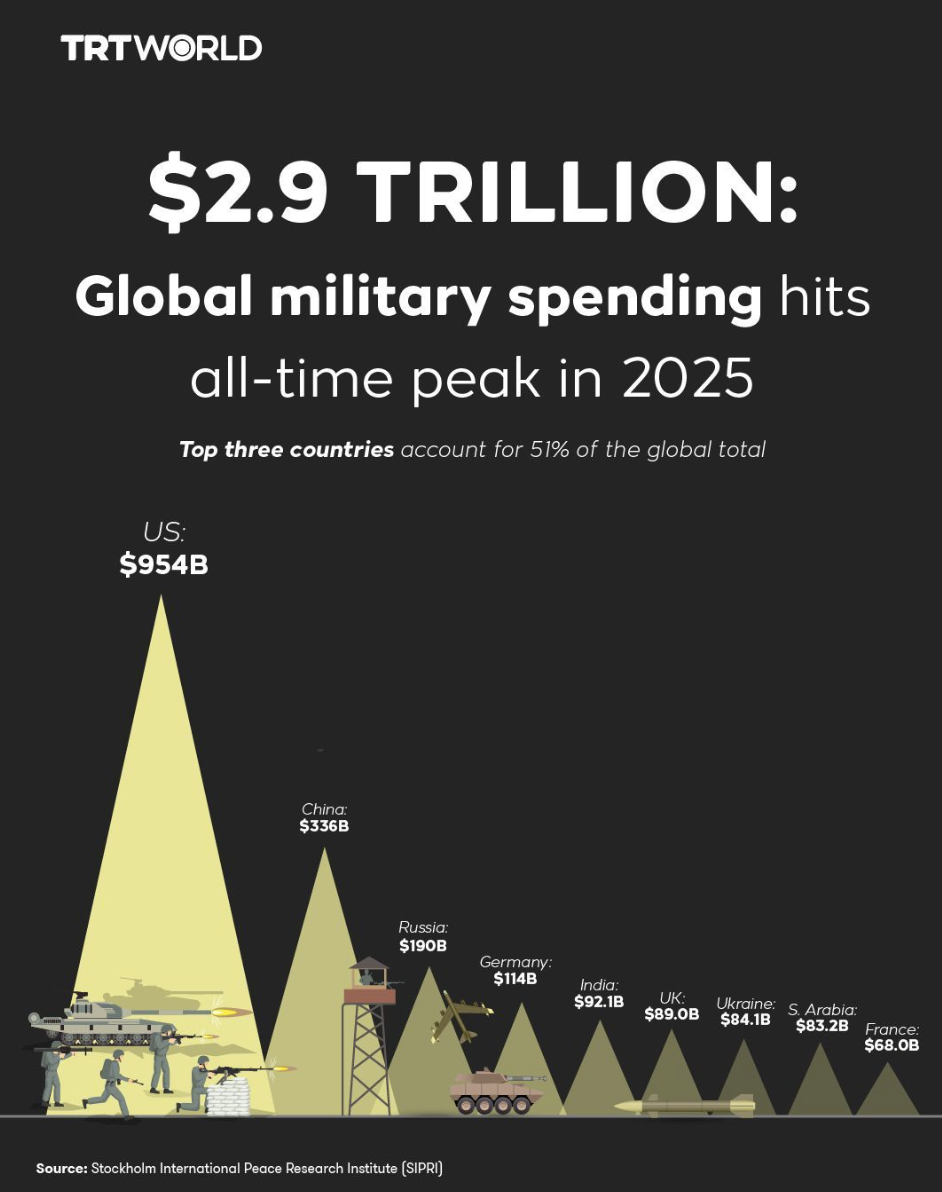

Global military spending reached $2.9 trillion in 2025, reflecting rising defence budgets, fragmented security dynamics, and growing risks to global peace.

Global military expenditure has reached a new high, rising by 2.9 per cent in 2025 to approximately $2.9 trillion. This marks the 11th consecutive year of growth and represents 2.5 per cent of global GDP, the highest share since 2009.

The headline figure suggests continuity rather than acceleration, particularly given that the annual increase is smaller than the sharp surge recorded in 2024. However, beneath the aggregate data lies a more consequential shift in the global security landscape. While the United States, still the world’s largest military spender, reduced its expenditure by 7.5 per cent due to a pause in new aid to Ukraine, spending by its allies, particularly across Europe and NATO, rose significantly.

This redistribution of military investment reflects a deeper structural transformation that aligns closely with the trends identified in The Great Fragmentation report, which looks at the rise of Middle Powers in a fractured international order: a world becoming more fragmented, less predictable, and increasingly reliant on hard power to manage insecurity.

European defence budgets rose by double digits in 2025, driven largely by the ongoing war in Ukraine and uncertainty over long-term US security guarantees. This reflects the transition from a rules-based order dominated by a small number of powers, to a more fragmented system characterised by regional blocs and middle powers. In such an environment, military capability becomes a key instrument of national resilience.

At the same time, rising tensions in Asia and Oceania, where military spending increased by over eight per cent, point to growing strategic competition, particularly around maritime security and territorial disputes.

The result is a global arms dynamic that is less about a single arms race and more about multiple, overlapping regional security dilemmas.

The decline in US military expenditure in 2025 highlights a redistribution of the security burden. The US remains by far the largest military spender, accounting for roughly one third of global expenditure, and any short-term reduction is likely to be temporary. However, the reduction has accelerated efforts by allies to increase their own capabilities. NATO countries, in particular, have moved decisively towards higher defence spending targets, with some considering levels well above the long-standing two per cent of GDP benchmark.

This shift is consistent with the Global Peace Index 2025 (GPI) findings that global security is becoming more decentralised. Countries are increasingly investing in their own deterrence capabilities rather than relying on collective security frameworks. While this may enhance national resilience in the short term, it also risks reinforcing cycles of mistrust and escalation.

The GPI highlights a continuing deterioration in global peacefulness, driven by intensifying geopolitical competition, rising conflict intensity, and growing distrust between major powers. These dynamics are directly feeding into higher defence spending. As the global order becomes more multipolar, states are placing greater emphasis on self-reliance in security, rather than depending on traditional alliances or multilateral institutions.

The Global Terrorism Index 2026 provides additional context for the rise in military expenditure. Although global terrorism deaths have declined overall, the threat has become more concentrated and geographically uneven. Regions such as the Sahel and parts of sub-Saharan Africa have experienced sharp increases in terrorism-related violence, while other regions have seen improvements.

This divergence creates complex policy challenges. In many cases, rising military spending is a response not only to interstate tensions but also to persistent internal security threats. For example, Nigeria’s military expenditure rose sharply in response to escalating insurgencies, even as global terrorism trends improved. However, the GTI consistently shows that military responses alone are insufficient to address terrorism.

High levels of militarisation, particularly when accompanied by human rights abuses or weak governance, can exacerbate the conditions that enable extremist recruitment. The GTI identified that a majority of recruits in at risk regions cite state violence or lack of economic opportunity as key drivers for joining extremist groups. So while military spending may be necessary to contain immediate threats, it does not address the underlying drivers of conflict.

The sustained rise in military expenditure also raises important questions about opportunity costs. With global military spending approaching $3 trillion annually, the allocation of resources towards defence has implications for economic development, social cohesion, and long-term peacebuilding. The GPI details the concept of Positive Peace, which refers to the attitudes, institutions and structures that sustain peaceful societies. These include well-functioning government, equitable distribution of resources, and strong business environments.

In many countries, increased military spending risks crowding out investment in these areas. This is particularly concerning in low and middle-income countries, where resources are already constrained and where investments in education, health, and economic opportunity can have a significant impact on reducing conflict risk. The global military burden reflects a shift in priorities at a time when many countries are also facing economic pressures, climate risks, and social inequalities.

Balancing these competing demands will be a central challenge for policymakers in the coming decade.

The current trajectory of global military spending suggests that the world is entering a period of sustained militarisation, a heightened level of strategic competition and a reduced capacity for cooperative security at a time when conflict is becoming more complex, more fragmented, and more difficult to resolve. In this context, rising military expenditure is both a symptom and a driver of declining peacefulness.

While investment in defence may be justified by legitimate security concerns, it is not a substitute for the broader conditions that sustain peace. Without parallel investment in peace, the risk is that higher military spending will reinforce the very insecurities it seeks to address.

The economic priorities of Sudan are distorted by the conflict. Sudan is a relatively poor country that spends far more lavishly on guns than on...

The single largest component of the economic impact of violence was global military expenditure, which totalled $8.4 trillion, or 44% of the total...

Identifying and measuring the factors that drive peace